BANKING ON LOVE : THE IDEAL NUMBER OF ACCOUNTS FOR COUPLE'S FINANCIAL HARMONY

- Mon Sep 15 18:30:00 UTC 2025

- In CASE STUDIES by Aparna Bose

Case Study : Number of Bank Accounts That Couples Should Have

Money is one of the most important aspects of married life. While love, trust, and companionship form the foundation of a relationship, financial planning provides the stability to build dreams together. One of the simplest yet most powerful steps couples can take is to structure their finances smartly using multiple bank accounts.

When Amit and Neha got married, they quickly realized that love wasn’t the only thing they needed to manage - money was a big part of their new life together. Both were earning professionals, but their spending habits were very different. Within months, they started facing friction. Amit loved investing in stocks and IPOs, while Neha trusted Mutual Funds and worried about emergencies and insurance. Add to that household bills, weekend dinners, and personal shopping - and suddenly, finances became a source of stress.

So, after several insightful sessions on investment and financial planning with our experts at Investaffairs instead of letting money divide them, they built a structured system with multiple bank accounts. Let’s see how things changed.

BEFORE THE THOUGHT-PROVOKING DISCUSSIONS : CONFUSION AND CONFLICTS

- Mixed - Up Expenses : Household bills, eating out, and personal shopping were all paid from a single account, making it nearly impossible to track where the money disappeared by month - end.

- Conflicting Goals : Amit leaned toward investing in the stock market, not bothering much about emergency funds while Neha prioritized building a safety net with Mutual Funds, health insurance and emergency savings - leaving both uneasy.

- Arguments Fueled by Guilt : Small remarks like "You spent too much on clothes" or "Why did we splurge on Zomato again?" often snowballed into avoidable quarrels.

AFTER THE THOUGHT - PROVOKING DISCUSSIONS: CLARITY AND EQUILIBRIUM IN PERSONAL SAVINGS ACCOUNTS

Accounts that were modified and decided upon :

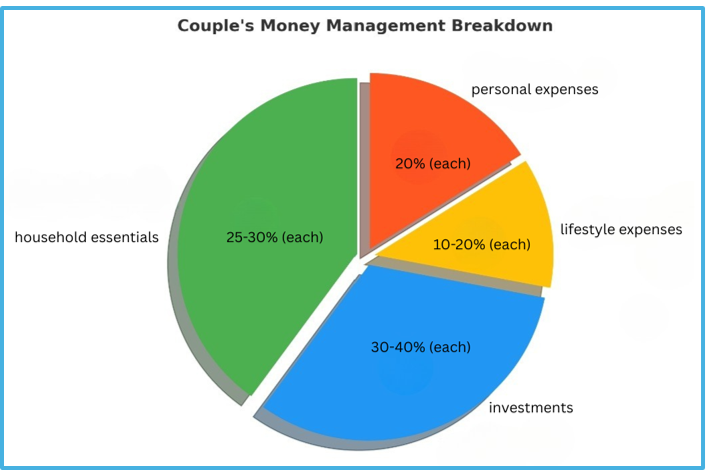

Individual Savings Accounts

20% of income (each) – to be reserved for personal spending.

Result: No more guilt or questions over coffee dates, online shopping, or hobbies. Each had financial freedom.

Joint Account (Lifestyle Expenses)

They opened a joint account where both will contribute proportionally.

10 - 20% of income (each) would go here.

To be used for: Vacations, dining out, movies, and other shared experiences.

Result: No more "who pays this time?" - all lifestyle expenses were covered fairly.

Individual Investment Accounts

They created separate investment-focused accounts based on their financial styles.

Amit’s portfolio: Stocks, real estate, SIPs.

Neha’s portfolio: Mutual Funds, gold, silver, term insurance, health insurance, emergency fund.

30-40% of income (each) to be invested.

Result: A healthy mix of growth and security.

Joint Account (Household Essentials)

They committed 50% of combined income (25-30% each) to cover rent, groceries, bills, kids’ fees (in future), and EMIs.

Result: Essentials were never compromised, and lifestyle expenses didn’t eat into basic needs.

TRANSFORMATION

The transformation was remarkable. What once felt like monthly confusion, tense discussions over spending priorities, and lingering anxiety about savings turned into a transparent system with clear buckets. This new approach fostered both independence and joint responsibility, brought peace of mind knowing that essentials and future goals were secured.

![]()

WHY THIS SYSTEM WORKS !

- Transparency – Both partners know where the money is going.

- Financial Freedom – Each retains autonomy over personal spending.

- Shared Responsibility – Household and lifestyle expenses are jointly managed.

- Future Security – Investments and insurance provide a safety net for the family.

Here’s a pie chart infographic that visually explains the couple’s money management strategy:

KEY TAKEAWAY FOR COUPLES

Managing money as a couple isn’t about giving up control or micromanaging each other— The right bank account structure ensures that both partners grow individually while also working toward common goals. By setting up individual savings, joint spending, and investment accounts, Amit and Neha turned money from a source of stress into a tool for security and happiness.

By dividing income smartly into savings, investments, joint expenses, and personal freedom, couples can enjoy the best of both worlds—Financial Discipline and Lifestyle Enjoyment.

Disclaimer: The data and information has been sourced from various domains available to the public. We have taken utmost care to represent the same as factually as has been made available. Please do not make any decisions based on our blogpost. Kindly check the data & information independently. For further guidance on finance and investment please reach out to our experts at Investaffairs.

If you have any Personal Finance query, do write to us

Categories

Recent Posts