THE HIDDEN COST OF LIVING LONGER: WHY MEDICAL INFLATION CAN DERAIL YOUR RETIREMENT

- Thu Nov 06 18:30:00 UTC 2025

- In personal finance by Aparna Bose

In an era where living longer has become the norm, the real challenge isn't just about adding years to life, it's about staying financially healthy through those extra years. What many overlook in their investment planning is medical inflation-the silent force eroding savings and threatening retirement security.

In our opinion, depending solely on employer-provided health insurance (salaried people) is risky. Therefore, proactive budgeting and personal finance management through disciplined investing and adequate health cover is key to true financial freedom.

REDEFINING A COMFORTABLE RETIREMENT: HEALTH AND PURPOSE FIRST

When individuals think of "retiring rich," they frequently envision a life of luxury filled with beach houses, travel, and relaxation. However, genuine retirement comfort relies on two fundamental elements: Health and Purpose.

Oftentimes chronic illnesses or unexpected medical emergencies can quickly deplete savings, often more rapidly than any market downturn. The foundation of a solid retirement plan begins with prioritizing your physical and mental health.

Conversely, having a sense of purpose is just as important. Approaching retirement as a continuous vacation can foster boredom and feelings of depression. Remaining engaged through hobbies, volunteering, or exploring new opportunities helps maintain a sense of meaning in life and keeps the mind active.

FROM RETIREMENT TO FINANCIAL FREEDOM

It's time to change how we think about retirement or dotage. The word itself often feels heavy-final, grey, and uninspiring. But what if we replaced it with something more empowering? Let's call it "Financial Freedom".

This shift in language transforms your mindset. Thinking of saving and investing as steps toward freedom makes the process exciting instead of intimidating, leading to a future you truly look forward to. However, a significant threat to financial plans is medical inflation, especially in India, where healthcare costs have risen nearly twice as fast as general inflation. Hospital stays, medications, and treatments are becoming increasingly expensive.

Many employees mistakenly believe their company's health insurance is sufficient. Unfortunately, employer plans often have coverage limits and may end at retirement. It's crucial to establish your own independent health coverage early, when premiums are more affordable and you're likely in good health.

That's why, at Investaffairs, we always ensure your investment portfolio includes provisions for medical insurance premiums, elderly care and caregiver expenses.

ASSESSING THE 4% WITHDRAWAL RULE IN THE INDIAN CONTEXT

The "4% rule," a popular guideline in retirement planning, was developed in the U.S. and indicates that retirees can withdraw 4% of their investment portfolio annually without depleting their funds. However, using this rule directly in India may be deceptive. Variations in inflation rates, market fluctuations, and the availability of long-term data suggest that a more conservative withdrawal rate in India would be between 3% and 3.5%.

The most important factor to monitor is your real return-the difference between your portfolio's returns and your personal inflation rate.

For instance, if your investments generate 12% and your household inflation is 6%, your real return stands at 6%. Aligning your annual withdrawals with this real return helps preserve your capital and provides stability throughout retirement.

That said, there is no "one-size-fits-all" formula for building wealth through mutual fund investments. This is where Investaffairs sets itself apart from other MFDs. We believe in a boutique approach-considering every aspect of your financial life to create a tailor-made retirement strategy crafted by our experts to suit your unique goals and circumstances.

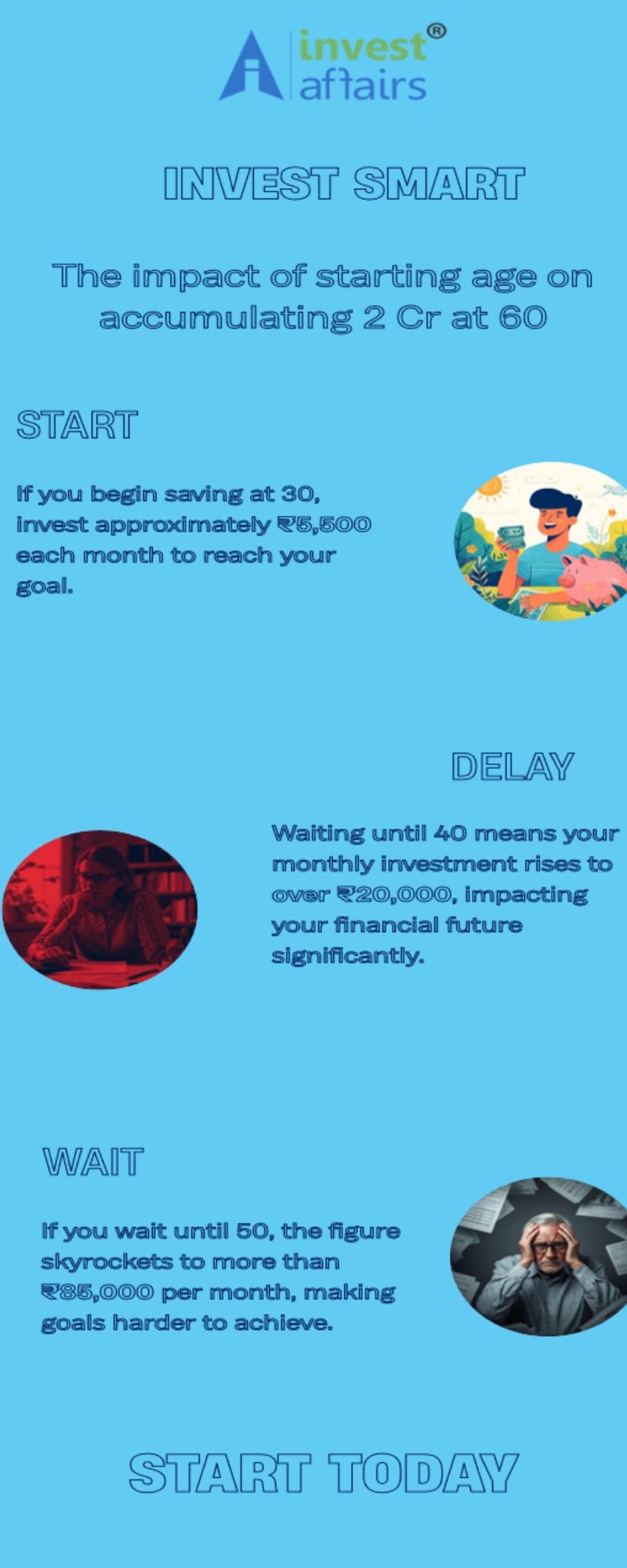

THE PRICE OF PROCRASTINATION: WHY RETIREMENT PLANNING CAN'T BE PUT OFF

In India, where social security systems are limited, delaying retirement planning can have severe financial consequences. Consider this (infographic)- This illustrates the cost of delay and emphasizes why initiating your retirement planning early not only provides financial advantages but also allows you the flexibility to enjoy your present while preparing for the future.

For many individuals in their 30s and even 40s, retirement often seems like a far-off issue. We tend to believe there will be time to address it later. This tendency to procrastinate is not just prevalent in India; it's a common human behaviour. People are naturally inclined to respond to immediate dangers-those that are tangible. In contrast, future threats, such as retirement, geopolitical events affecting growth and inflation, supply chain vulnerabilities, climate change, and workforce instability, often feel abstract, leading us to overlook them.

BUILDING A BALANCED RETIREMENT PORTFOLIO

Equity is a powerful tool for long-term wealth creation, but experts caution against relying on it alone-especially near retirement. While equities offer strong returns, their volatility can hurt your corpus if markets fall early in retirement. Diversifying across equity, debt, and hybrid funds is essential.

With longer lifespans, one major challenge is rising healthcare costs. Many plan for wealth, homes, or education but overlook medical inflation-a growing threat to a secure and stress-free retirement.

FINAL THOUGHTS

Retirement planning isn't just about numbers-it's about mindset. Start early, stay healthy, invest wisely, and plan for purpose as much as for prosperity. Relying solely on employer-provided health insurance isn't enough. Proactive planning-through adequate health cover and disciplined investing-is no longer optional; it's essential. Because in the end, financial freedom isn't about how much money you have-it's about how much peace you enjoy while using it.

Disclaimer: The data and information has been sourced from various domains available to the public. We have taken utmost care to represent the same as factually as has been made available. Please do not make any decisions based on our blogpost. Kindly check the data & information independently. For further guidance on finance and investment please reach out to our experts at Investaffairs.

If you have any Personal Finance query, do write to us

Categories

Recent Posts